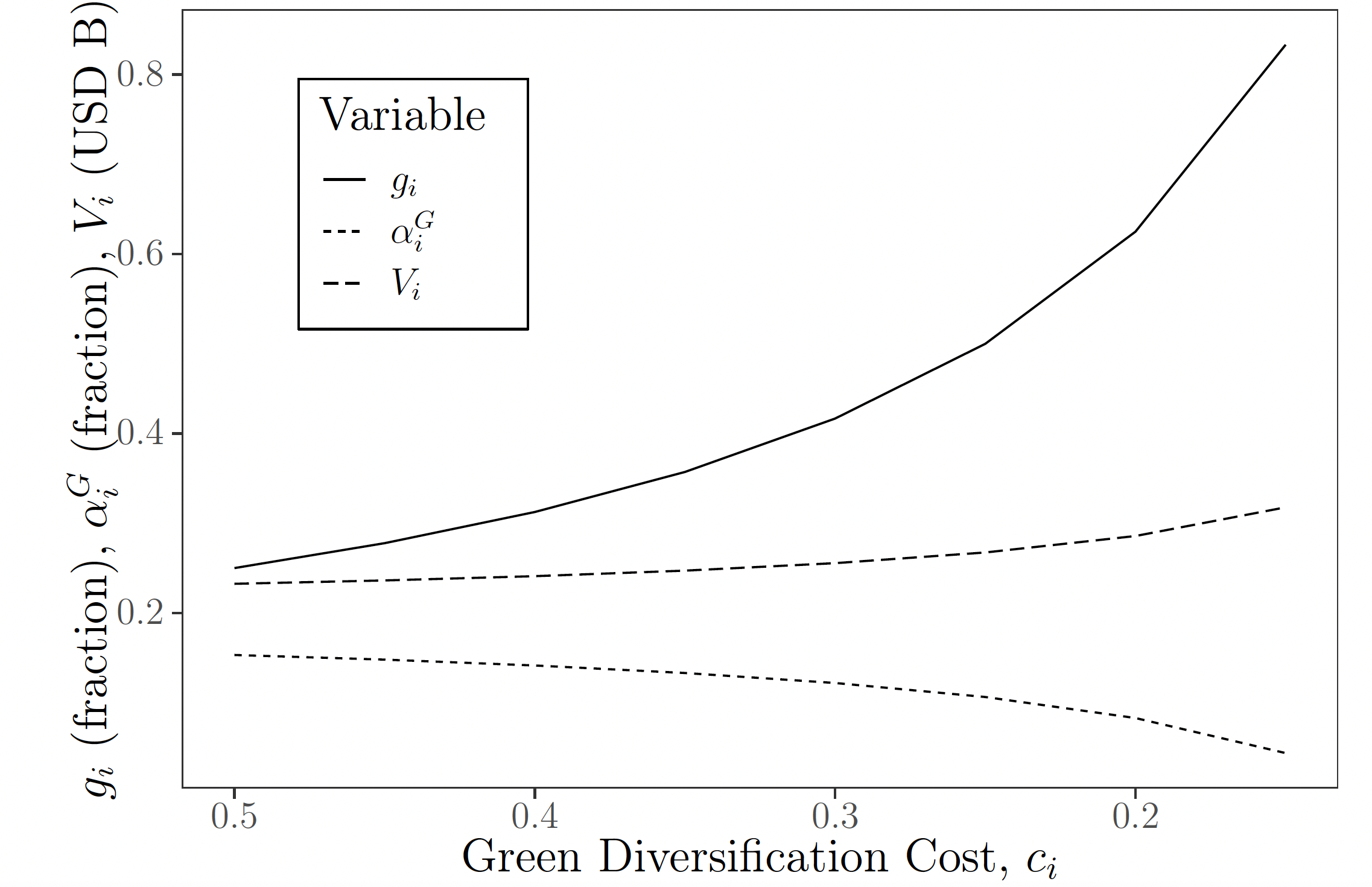

When countries increase their macroprudential buffer it increases the price of risk in their respective economies.

Presented at: Wharton School at the University of Pennsylvania, PhD Nordic Finance Workshop, Poster Session at American Finance Association Annual Meeting (AFA), Copenhagen Business School.

I document that equity prices fall as macroprudential buffers are announced. This is consistent with macroprudential buffers leading to an increase in risk premia, from a heightened price of risk. Theoretically, I develop a model that predicts that as buffers are announced 1) The price of risk increases, 2) Systemic risk falls, and 3) Intermediaries' risky asset allocation decreases, as other agents with higher risk aversion increase their portfolio weights in the risky asset. Empirically, I find evidence consistent with the first and third prediction. The second remains a testable implication of my model. In summary, this paper sheds light on the equilibrium effects of implementing new financial regulation on asset prices and systemic risk.